An insurance claim is a formal request that you submit to your insurance company for coverage or payment under your policy. Whether it’s a car accident, property damage, or a health-related incident, filing a claim is absolutely crucial to getting the financial help you deserve. Understanding how the system works can help reduce the anxiety that can sometimes accompany negotiating the insurance system. Whether your claim is processed quickly and efficiently depends largely on information and preparation.

Gather the Necessary Facts and Documents

You should gather all the relevant documents and information before you file your claim. This includes a copy of your insurance policy, photos of the damage (if applicable), receipts or invoices, and any police records (if necessary). For example, if you’ve been involved in a car accident, photos of the damage to the vehicle, contact information for witnesses, and the official accident report will all support your claim. Being organized and contactable can save you time and prevent delays in the process.

Notify your Insurance Company: Step One

Once you have the information you need, you should first notify your insurance company. Most companies have a deadline for submitting claims. Missing this deadline could affect your eligibility for compensation. Whether you call, email, or use an online portal, you can contact your insurance company through their preferred channel. Make sure you have basic information to hand, such as your policy number, details of the incident, and the type of claim you are making.

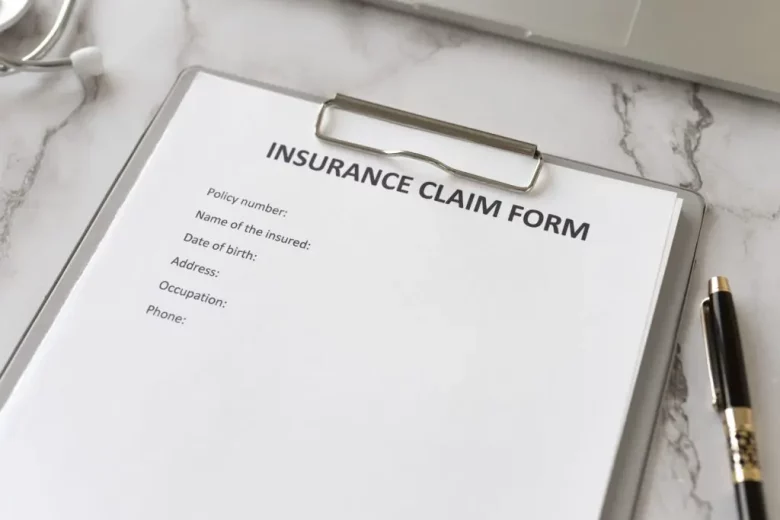

Fill Out the Claim form Correctly

Many insurance companies require you to fill out a comprehensive claim form as part of the process. This form is where you explain to your insurance company what happened and what the claim is about. It is essential that you fill out the form accurately. Include all necessary information, including support tickets, to avoid delays in processing. Check the information you enter for errors or omissions. Small errors can result in unnecessary correspondence between you and your insurance company.

Insurance Company Audit System

Once you file your claim, the insurance company begins assessing your claim. During this period, your insurance company checks the data entered to verify the authenticity of your claim and assess the costs or losses involved. To determine how much compensation you will receive, the insurance company also checks your policy coverage. The complexity of the claim determines how long this phase lasts: a few days or a few weeks. Regular follow-up can help you be proactive and patient so that your problems do not go unnoticed.

Dealing Effectively with Insurance Company Claims Adjusters

For certain claims, your insurance company may appoint a claims adjuster to assess the extent of the damage and negotiate a settlement. As a representative of the company, the adjuster assesses the damage and discusses future actions. Approach the adjuster in an open and cooperative manner. Record all communications and ensure that all requested data is sent as soon as possible. If possible, you can go to a claims adjuster to explain your situation in person.

Understand Your Policy Coverage and Exclusions

You need to be completely clear about your policy before and during the claims process. Policies typically contain extensive coverage limits, exclusions, and conditions that determine your claim amounts and coverage circumstances. For example, flood or earthquake coverage may require additional coverage, while health insurance may not cover pre-existing conditions. Reviewing these clauses can help you set reasonable expectations and avoid surprises after a claims decision is made.

Negotiating a Settlement: Tips and Tricks

If the insurance company’s compensation package doesn’t meet your expectations, don’t hesitate to negotiate. Start by reviewing the adjuster’s estimate, then check it against your own records. Be prepared to point out any evidence-based discrepancies or underestimations. It keeps people calm, professional, and resilient throughout the process. If you find yourself in trouble, consider hiring a public adjuster or attorney to help you negotiate a reasonable settlement.

Appealing a Rejected Claim: Next Steps

If your claim is denied, the path to legal action is not closed. Insurers give a variety of reasons for refusing to pay, ranging from policy exclusions to lack of evidence. Start by carefully reading the denial letter and comparing its specific contents with your policy. Your insurance company should be able to provide you with a detailed explanation of this as well. If you believe your claim has been wrongly denied, gather more information and file a formal appeal through the company’s procedures. It may also be helpful to seek help from a consumer protection agency or ombudsman.

Preventing Future Claims: Best Practices

Good organization and proactive planning are the first steps to preventing future claim-related problems. Review your insurance regularly to ensure you have adequate coverage, especially if your circumstances change—whether you move, buy a new home, or experience a life event. Keep accurate records—photos, receipts, maintenance logs—that will certainly support your claim. Finally, report the incident as quickly and accurately as possible to meet the insurance company’s standards.

Conclusion

While handling an insurance claim can seem daunting, by describing the process step by step, you can find a reasonable approach. Good preparation, policy awareness, and proactive, phased behavior greatly increase the likelihood of a positive outcome. By following these tips, you will receive the compensation you deserve, whether it’s a minor issue or a major accident. If you have questions or need professional assistance with your claim, contact an insurance professional. They can help you through the process.

FAQs

1. How long does it take to process an insurance claim?

The type and complexity of the claim will affect the timeline. Some issues can be resolved in a few days, while others can take weeks or even months.

2. What if I disagree with the insurance adjuster’s findings?

You can refute the report with additional information or evidence. If necessary, you may consider consulting a public adjuster or attorney.

3. Do I need to notify the insurance company immediately after the accident?

Most policies have a time limit for recording incidents. Delays can result in your claim being denied. Therefore, we recommend that you notify your insurance company immediately.

4. Can I still file a claim if I do not have all the necessary documentation?

That is true, but thorough and accurate record-keeping speeds up the process and increases the likelihood of success.

5. What happens if my claim is denied?

If necessary, seek outside mediation or legal assistance. Otherwise, you can appeal the decision to your insurance company and provide additional evidence.